The governance and origins of Bitcoin closely resemble those presented in the founding documents of the United States.

This is an opinion editorial by Buck O Perley, a software engineer at Unchained Capital helping build bitcoin-native financial services.

This is Part Two of a two-part article set that describes crypto-governance and the dangers of faction. Part one can be found here.

What Does All Of This Have To Do With Cryptocurrency?

Most of this discussion so far has been theoretical. A lot of it has been about the nature of humanity and how that should be considered when devising governance schemes. What I’d like to do though is to try and tie this into cryptocurrency as it is presently thought about and implemented (or should be), and I’d like to touch on this in two respects.

The first is how I believe the structure of the Bitcoin ecosystem, including much of its political divisions, reflect the ideas and concerns outlined above by the U.S. founders and other Enlightenment thinkers, and how this is one of its greatest strengths.

Second, I will look at the ongoing block size and hard fork debate that has been raging for the past two years.*

*Editor's note: Part One of the series details that this article was originally written in 2017.

I make no claims to Bitcoin being a perfect implementation of human governance in code or for being a Bitcoin maximalist. I am simply making a comparison between the two systems and how the parallels lend themselves to Bitcoin’s strengths.

Bitcoin’s Checks And Balances

Comparing Bitcoin to the United State’s system of government is not a new idea, but I think it bears repeating in the context of the philosophy that gave birth to that system as outlined above.

First are the remarkable number of parallels between the contexts in which they came about. Neither was the first attempt at a radically different view of human liberty (non-governmental, digital currencies had been worked on for decades prior to the advent of Bitcoin) and thus reflect many decades of work, research and thought. Both were launched in response to what their respective creators viewed as overreaches of the prevailing systems they would later seek to subvert and both came about in adversarial circumstances such that every contingency had to be taken into account in order to assure their respective survivals.

The Declaration of Independence was an airing of grievances against the crown and a declaration of intention of the colonies for self-governance. Similarly, in Satoshi’s original white paper, the inadequacy of our legacy payment systems are laid out and a proposal for rectification put forward.

Just as the Constitution and Bill of Rights were the realizations of the vision put forward in the Declaration, so too was the open-source reference implementation of Bitcoin the realization of the ideas from the white paper by Nakamoto. In another parallel, neither remained in their original form with both subject to needed change (Amendments for one, Bitcoin Improvement Proposals, or BIPs, for the other).

For the past 20–30 years we have been used to thinking of code as a product. Even open-source projects are often run as if they are proprietary, just with more transparency. Maintainers decide the road maps, choose which changes do and don’t get incorporated, and address (or ignore) the issues of the users at their discretion. Code, like laws, can be changed and as code increasingly comes to take on more of the responsibilities previously handled by laws (read Nick Szabo’s writing on “wet” vs. “hard” code for more on this) it is important to consider how changes can and should be affected.

So how does this work in a distributed network where a code change often isn’t as simple as an automatic upgrade to your iPhone? How do you account for a system meant to take a diversity of opinions and priorities into account, where it’s not clear who has the “right” answer, and how do you coordinate changes where if the network isn’t in unanimous agreement it suffers a split that can cause real financial harm?

Just as the U.S. Founding Fathers devised mechanisms to allow for change in a system absent an absolute ruler, so too did Satoshi Nakamoto take this problem into account:

“The proof-of-work also solves the problem of determining representation in majority decision making. If the majority were based on one-IP-address-one-vote, it could be subverted by anyone able to allocate many IPs. Proof-of-work is essentially one-CPU-one-vote. The majority decision is represented by the longest chain, which has the greatest proof-of-work effort invested in it.”

The analogy would be:

Proprietary code = absolute dictatorship.

Open-source projects for non-distributed systems = parliamentary monarchy.

Decentralized consensus networks (like Bitcoin) = constitutional republic (or popular democracy depending on the implementation).

“If men were angels, no government would be necessary. If angels were to govern men, neither external nor internal controls on government would be necessary.” — James Madison, Federalist No. 51

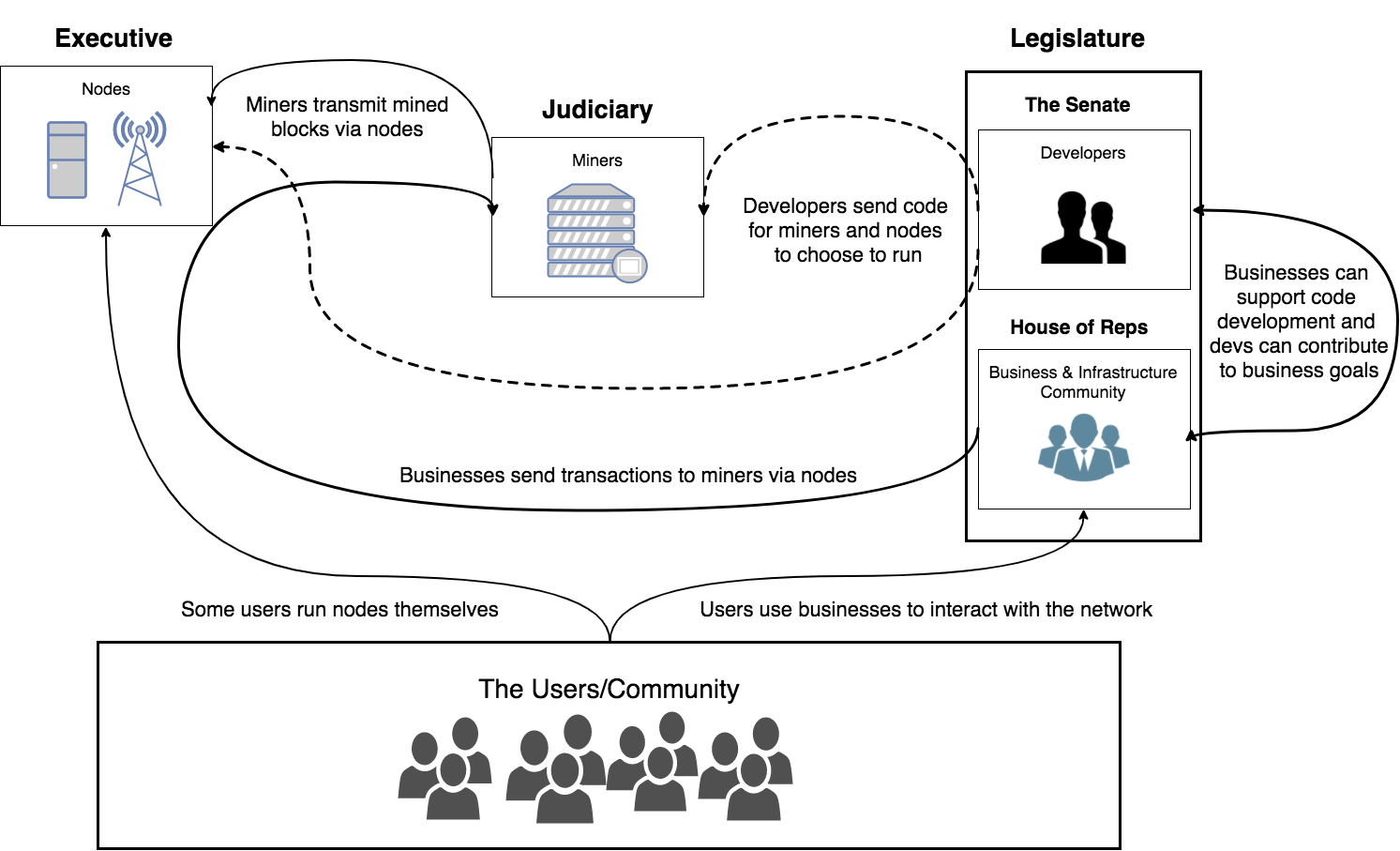

The Branches Of Governance

The system of checks and balances devised by the founders represented an important mechanism to both enable governance while also inhibiting overreach from any of the competing branches of government.

In Bitcoin, full nodes are those “participants” in the network that contain the full history of the blockchain and the verified unspent transaction outputs (UTXO) set that are needed to verify transactions. Like the executive branch of the U.S. government, it is their job to “faithfully execute” the rules of the underlying protocol and “to the best of [their] Ability, preserve, protect and defend” the network.

Next up is the proof-of-work security provided by miners. While they don’t make the rules, similar to the American judiciary, miners enforce the rules of the network and ensure its continued smooth operation. Without the security brought by miners to the transmission of transactions, the value of the underlying token (e.g., bitcoin) decreases thus decreasing the value of the rewards they receive for bringing the security in the first place. This is a dual incentive relationship that undergirds much of the game theory for most stakeholders in the system.

Finally, we get to the third branch of a constitutional republic — the legislature. Much as in the U.S. system, this has evolved into a two-pronged, and sometimes competing, structure. Playing the role of the House of Representatives are the entrepreneurs, businesses, infrastructure developers (wallets, graphical interfaces) and investors. Like their government counterparts in the U.S., these will tend to be the most “democratic” of the branches representing the widest diversity of viewpoints as they are in more regular and direct contact with everyday users of the currency. Some conflicts may arise in the area of short-term profits versus long-term health of the system, but, overall, businesses both bring long-term viability to the network by providing services such as exchanges, marketplaces, wallets and accessible security and most benefit the more useful the currency becomes in the long term.

The final arm of the legislature in the U.S. system is the Senate, a role played in Bitcoin by the developers. As originally envisioned by the founders, this chamber was meant to be one more step removed from the people than the House of Representatives as they were elected by the state legislatures (until the very misguided 17th Amendment which transitioned to direct popular election of Senators and is likely a large contributor to our present increased partisanship and misguided populist movements). Similarly, developers can be supported by companies in the ecosystem or can contribute from their own free time. Much of their authority comes from their experience in the industry.

A very rough and simplistic diagram of Bitcoin’s governance model.

The incentives of developers, however, are less straightforward than the other “branches.” Value for them is derived from two primary sources — first are any holdings of the cryptocurrency token (bitcoin) which they already hold and will correspondingly be worth more as the utility of the token and demand for it increase and second is the power and influence that comes with being a lead developer for a project worth billions of dollars.

This comes with three areas of asymmetric incentives.

First is that developers are the only economic stakeholders (aside from full nodes which play a purely passive role in the system) that do not earn more of the underlying token that they are supporting. This skews incentives towards incumbents being more conservative (not necessarily a bad thing, especially as it can counterbalance any tendency towards short-termism of businesses) as they benefit from the value of their holdings increasing — something that can be manipulated with the perception of value — rather than increased utility. This can result in its own form of more narrow, short-term thinking.

Second is it incentivizes the crowding out of new developers from entering the space as the bias is towards incumbents. Developers are attracted by interesting projects and welcoming environments and, in fact, more short-term profits can be realized by new developers who move to newer projects where the potential short-term gain from the launch of a new cryptocurrency token is much higher. Incumbent developers meanwhile are incentivized to have their proposals take precedence while also being incentivized to increase complexity which further increases the barrier to entry of competing and newer developers entering the space (thus further increasing the value of their expertise).

The final risk of this incentive scheme is the potential to foster cults of personality. As experience becomes more concentrated and more scarce, there can be a tendency to put trust in the hands of those who we believe are the most altruistic, doing things for the longest time for the good of the system. The problem though, in the words of C.S. Lewis, is:

“Of all tyrannies, a tyranny sincerely exercised for the good of its victims may be the most oppressive. It would be better to live under robber barons than under omnipotent moral busybodies. The robber baron’s cruelty may sometimes sleep, his cupidity may at some point be satiated; but those who torment us for our own good will torment us without end for they do so with the approval of their own conscience.”

This comes with the added risk that it makes the “citizens” of that system dangerously complacent towards leaders with whom they agree, and more antagonistic and partisan towards those with whom they disagree, dividing the community further by rewarding and promoting the loudest, and usually more extreme voices (something the U.S. and much of the world is currently experiencing as well).

Again, the lesson of the U.S. founders is that all power must be distrusted, no matter how good the motives. Conversely, differing opinions should be welcome or at least understood to be inevitable and do not necessarily come from malicious motives.

The last piece of this comparison has to do with the mechanisms for change. As outlined earlier, it should be hard to make changes in a governing system. In the words (again) of Calvin Coolidge: “It is much more important to kill bad bills than to pass good ones.” In Bitcoin these mechanisms take two forms — first are forks (both soft and hard forks) for implementing changes and second is the proof-of-work difficulty adjustment for making any contentious change expensive.

The difficulty adjustment essentially acts as Bitcoin’s barrier to overcome for “Constitutional Amendments” (i.e., protocol updates) in order to be passed ( deployed to the network). The way proof-of-work difficulty works as a disincentive is that without a supermajority of mining power and an economic majority backing it, the rate of blocks mined can drop precipitously which means that the rate at which transactions can be confirmed also drops and thus the utility of the coin itself goes down (usually though not necessarily leading to the value also decreasing, which often depends on the motivation behind the fork, i.e., forks viewed as malicious or untrustworthy are less likely to hold higher value). The difficulty for mining new blocks adjusts based on a target of a new block being mined on average every 10 minutes. If there are more computers mining Bitcoin, the cryptographic difficulty goes up in order to maintain this average, and down if miners leave. This “retargeting” only happens every 2,016 blocks though, which means that a fork with a significant minority of hash power could be stuck at hour-long wait times for weeks or even months.

This makes the cost of a fork without significant buy-in from more than one branch of the governance system prohibitively expensive. Several upgrade proposals such as BitcoinXT, Bitcoin Classic and Bitcoin Unlimited had some buy-in by miners (never over 40% though) and very little from the business ecosystem or developers and thus never activated. Segregated Witness was an upgrade deployed on the network by the Bitcoin Core developers in 2016, but, due to a lack of mining support (never much more than 30%) stemming from a distrust some held towards the developers most vocally in support of the change, it went a year without activation. It was finally activated only after some “parliamentary” shenanigans, a compromise between the business community, some developers and miners for a later hard fork in exchange for activation and threats of a “user-activated soft fork” initiated by full nodes on the network which promised to reject blocks from miners not in support.

It wasn’t until Bitcoin Cash forked in August 2017 that a contentious fork was finally executed and sustained a split. Notably though, in order for their fork to survive, they had to change proof-of-work retargeting so that miners would be able to find blocks faster than the default retargeting time would allow. This resulted in some crazy price swings and price manipulations by miners jumping between chains making the chain less reliable and its token less valuable. And even with the change, Bitcoin Cash miners were losing money, hundreds of thousands of dollars by some counts, for the first couple weeks by forgoing mining on the main chain.

Most importantly to me though about the Bitcoin Cash fork is that by making it easier for a minority of miners to break off from the majority of the ecosystem, it is, therefore, easier for those in the future who want to similarly break off (which we now know with the benefit of hindsight is exactly what happened). This makes consensus essentially irrelevant and breaks one of the primary governance mechanisms of Bitcoin.

If it’s hard to fork and prohibitively expensive to impose contentious changes on the network, you are more protected from making bad decisions, more likely to be inclusive of differing opinions and more able to adapt for the long term regardless of whoever is governing in the short term. While forks can be harmful and disruptive to the network, the threat of forks is an important governance mechanism that should be respected and leveraged to make a more universal and inclusive system.

The Risks Of Factions

The final point I’d like to make on all this is an attempt to tie all of the above together with regards to how viciously partisan those in the community have become, seemingly to the point of religious fanaticism. Debating about what Satoshi Nakamoto’s “original vision” for Bitcoin was or that the Real Bitcoin™ is the one supported by some subset of the best known developers completely ignores the quite effective, and frankly proven, governing system that has been put into place.

Reasonable people can disagree while still having the best intentions for the network as a whole at heart. Character assassinations do nothing but divide the community to the point where, when you feel you have nothing left in common, the community decides it's better off splitting rather than coming to some common ground. It makes no sense to, on the one hand, say that the Real Bitcoin™ will be enforced by the economic majority and then at the same time say you will leave the community and sell all holdings if the economic majority chose a path you did not agree with. Price, utility, public perception and checks and balances that assume disagreement and lack of 100% consensus are demonstrably built into the governance mechanism.

If there is no way to deviate from a path that you may happen to agree with but the economic majority deems harmful to the network, then there is conversely no mechanism to defend against bad actors you do see as harmful. These mechanisms must be objective to the point where your side is equally capable of being a target of them. Anyone who thinks the experiment failed because their side lost is being dogmatic and ultimately leaves themselves open to tyranny. Instead, you should make your case as best you can and, after that, simply trust the system.

If you don’t trust the system, then we’ve already lost.

Jameson Lopp wrote a great article earlier this year on how no one can truly claim to know what the Real Bitcoin™ is. See these tweets that seem to be inspired from said post, “Nobody Understands Bitcoin (And That’s OK).”

Link to embedded Tweet one and two.

One Final Observation:

Satoshi Nakamoto Is Our George Washington

It is often taken for granted today how revolutionary it was at the time for George Washington to step down as the head of the U.S. government. When the news made it to Great Britain, Rufus King quotes King George III as saying that the resignation “placed him in a light the most distinguished of any man living, and that he thought him the greatest character of the age.”

Of course, in Bitcoin, we have experienced a similarly unique phenomenon, when, in 2010, after having been developing and helping to run the live Bitcoin network for two years, Satoshi Nakamoto’s online accounts went black. Not only that, but as the first and only miner on the network, Bitcoin addresses associated with Satoshi have funds that are today worth around $20.5 billion. The most remarkable thing is that these funds haven’t moved since Nakamoto went silent.

It is unclear why Nakamoto left the community or if it was even voluntary since we don’t even know who he/she is (while there are plenty of theories and there have been several “unmaskings,” none have been definitively proven and none have been widely accepted by the community). But what is clear is that like George Washington, Nakamoto left the Bitcoin ecosystem in a very unique circumstance. Just as it was unique for a person who was in a position to grab ultimate power to abstain from grabbing it (as Napoleon later would take power in France), Bitcoin remains the only major cryptocurrency where the creator is not just unknown but retains zero influence over the direction of the community. As outlined above, experienced developers hold an inordinate amount of power over the direction of a cryptocurrency, and none have more experience or influence than the original developers who can affect massive swings in the market with a simple announcement.

Ray Dillinger did one of the first code reviews and security audits of the Bitcoin code back in 2008, and he writes an incredible piece reflecting on how monumental what Satoshi built was and how unique it was that he left. In “If I’d Known What We Were Starting” he writes:

“[T]he Trustless nature of Bitcoin was the main thing that convinced me Satoshi wasn’t scamming. He built a highway with no toll bridge. People could use Bitcoin without creating any obligation to pay him anything ever. He wasn’t selling coins, he was giving them away for solving hashes. He reserved nothing for himself.”

“He wasn’t trying to line his own pockets at the expense of others. In fact I don’t think I’ve ever encountered someone so completely uninterested in personal wealth. You know the old saw about being able to get a lot done if you don’t care who gets the credit? Satoshi doesn’t want the credit. Two years later he walked away and left the pseudonym behind. And hard as this may be to believe, it looks like he doesn’t even want to be paid for it. As far as we can tell he mined approximately a million Bitcoins and has never sold a single one of them.”

Many decry the fractious environment that exists in Bitcoin today, but I would argue that much like how the messiness of political debate in a free society can feel exhausting when compared to the surface efficiency of authoritarian states, to abandon that messiness can also leave you vulnerable to the risks of tyranny itself, even one exercised for our own good. So while being without a uniting “supreme leader” may leave a community at each other’s throats, it is also important to remember that divisions are an opportunity to make us stronger as long as we avoid the temptation to view opposition as an existential threat and retain a sense of common purpose.

“The Mischiefs Of The Spirit Of Party” And “The Duty Of A Wise People”

This was a long essay series. If you made it this far, I commend you and thank you for bearing with me! There’s plenty I tried to address in here and hopefully at least some of it came across coherently enough to add something constructive to the discussion.

Unfortunately, it feels like Enlightenment political philosophy and the lessons of the founding of the U.S. have become increasingly niche areas of interest despite the immeasurable contribution they’ve made towards advancing human liberty across the world. Hopefully I was able to make the case for their relevance today even in as bleeding-edge a space as Bitcoin. In fact, as this technology leads us into a new stage of the evolution of human self-governance, it’s probably more important than ever to look back and reflect on lessons already learned but easily taken for granted.

To close off, I’d like to share George Washington’s remarks from his farewell address on September 17, 1796. In his speech, the first president devoted much time to a farsighted admonition against the dangers of faction and offered a sobering reminder of its consequences. It is a warning that I believe resonates even today and even in the crypto world (and especially in Bitcoin). It presents a strong and enduring indictment against the all too human temptation of putting “party” over principle and the damage this can ultimately inflict on liberty.

“The alternate domination of one faction over another, sharpened by the spirit of revenge, natural to party dissension, which in different ages and countries has perpetrated the most horrid enormities, is itself a frightful despotism. But this leads at length to a more formal and permanent despotism. The disorders and miseries which result gradually incline the minds of men to seek security and repose in the absolute power of an individual; and sooner or later the chief of some prevailing faction, more able or more fortunate than his competitors, turns this disposition to the purposes of his own elevation, on the ruins of Public Liberty.”

“Without looking forward to an extremity of this kind (which nevertheless ought not to be entirely out of sight), the common and continual mischiefs of the spirit of party are sufficient to make it the interest and duty of a wise people to discourage and restrain it.”

None of this is by any means a settled debate but hopefully it can become a more civil one. If you have any thoughts of agreement or contention I’d love to hear your comments and to further the discussion for a better and freer future!

This is a guest post by Buck O Perley. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

You can get bonuses upto $100 FREE BONUS when you:

💰 Install these recommended apps:

💲 SocialGood - 100% Crypto Back on Everyday Shopping

💲 xPortal - The DeFi For The Next Billion

💲 CryptoTab Browser - Lightweight, fast, and ready to mine!

💰 Register on these recommended exchanges:

🟡 Binance🟡 Bitfinex🟡 Bitmart🟡 Bittrex🟡 Bitget

🟡 CoinEx🟡 Crypto.com🟡 Gate.io🟡 Huobi🟡 Kucoin.

{kind=link}

Comments