“The only thing that’s certain is death and taxes.” This idiom may be overused, but adding a third item to that list is usually pretty clever.

For example, my editor would probably say: “The only thing that’s certain is death, taxes and a lot of misplaced commas that I have to edit out.” My personal favorite use comes from The Roots’ Tariq “Black Thought” Trotter’s freestyle where he says: “The only thing for sure is taxes, death and trouble.”

This week we’ll dive into the less-commonly used version of this phrase: “The only thing that’s certain is death, taxes and a whole bunch of off-base accounting rules governing the treatment of digital assets on corporate balance sheets leading to a misrepresentation of corporate earnings.”

That’s right, we’re talking about U.S. accounting rules this week. And right on cue, Tesla announced last Wednesday that it sold 75% of its bitcoin in the second quarter. So let’s dive in.

That (and maybe more …) below.

You’re reading Crypto Long & Short, our weekly newsletter featuring insights, news and analysis for the professional investor. Sign up here to get it in your inbox every Sunday.

Regrettably, we will first have to dive into the story everyone was squawking about on Wednesday so that we can cleanly set up a transition to our main accounting topic. That story is Tesla selling $936 million worth of bitcoin (BTC), which made up roughly 75% of its holdings.

Even more regrettably, I am sorta kinda coming to the defense of Tesla. Corporations are people too!

So it goes.

'I might pump, but I don’t dump'

Unlike what most of the internet wants you to believe, Tesla did not “paper hand” the bitcoin it bought last year for a loss. From Tesla’s second quarter earnings call:

“Additionally, we converted a majority of our bitcoin holdings to fiat for a realized gain offset by impairment charges on the remainder of our holdings, netting a $106 million cost to the [income statement].”

Not sure if you realize this, but a realized gain means Tesla realized a gain. And to realize a gain, you have to sell something for more than you bought it for. Otherwise, it would be a realized loss.

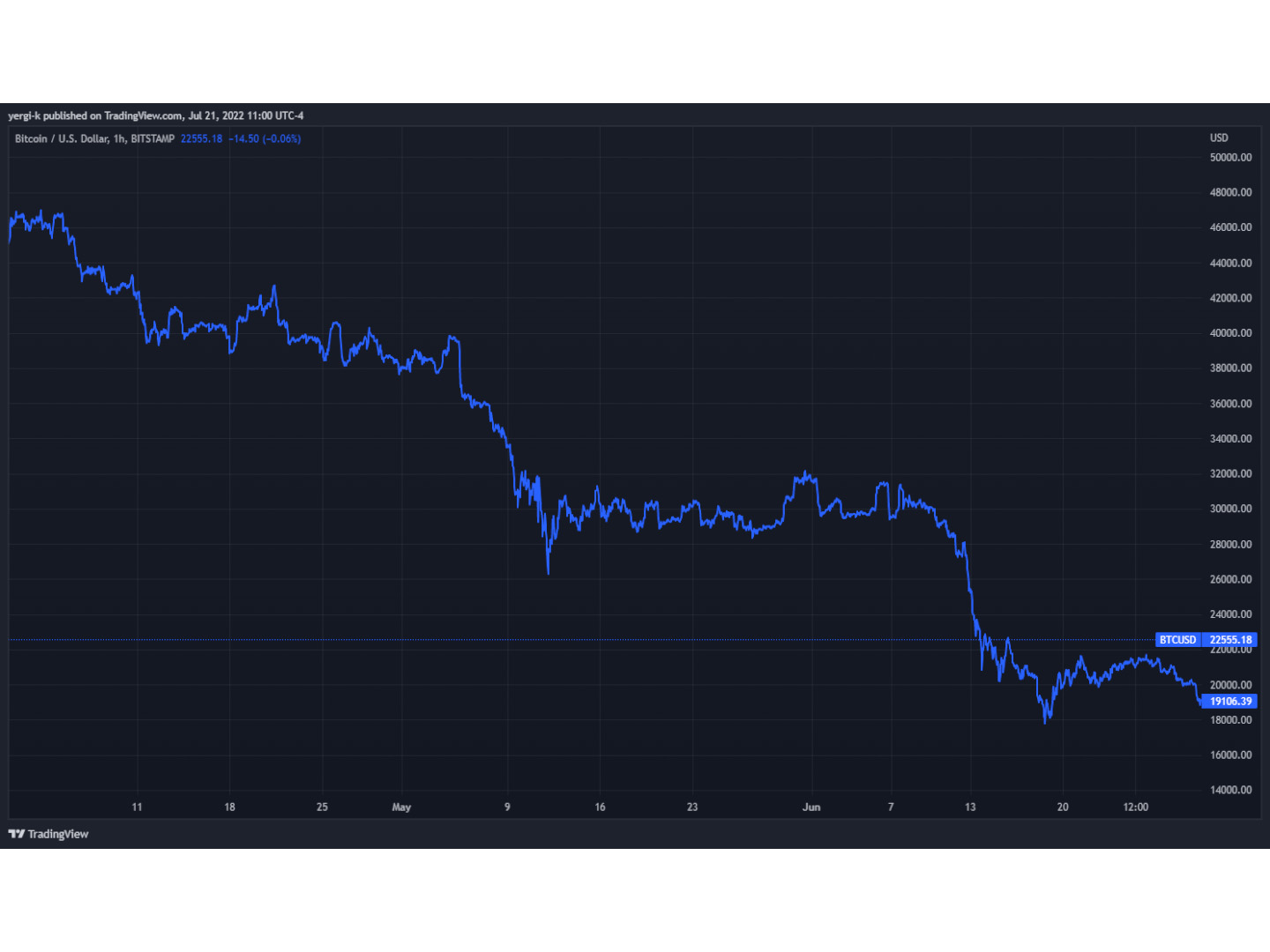

And when you realize that it made those sales sometime between April and June 2022, that’s when it gets a little interesting. For context, here is the price of bitcoin from April 1 to June 30, 2022

Bitcoin Q2 Price Performance (TradingView)

Bitcoin opened the quarter trading around $45,000 and ended it below $20,000. Somewhere in there, amid a lot of selling, is Tesla unloading some ~30,000 BTC. Also featured in this timeframe is the Luna Foundation Guard selling ~80,000 BTC during the UST/LUNA death spiral. That’s a lot of liquidity for the bitcoin market to soak up, and while it did cede 58% of its market capitalization, it didn’t cede 100% of it (a low bar, I know, but still).

Before we can dive into accounting rules, we need to highlight why Tesla sold any of its bitcoin at all. From the same earnings call:

“We were uncertain when the COVID lockdowns in China would alleviate so we sold bitcoin to bolster our cash position.”

Tesla’s most recent bitcoin sale is certainly not a critique of bitcoin. When Tesla sold some bitcoin last April it did so to “test liquidity.” Now, in the second quarter, when it needed cash, there was ample liquidity to supply that cash. So even though bitcoin was referred to as a “sideshow to a sideshow” on the call, Tesla’s CEO added that “we are certainly open to increasing our bitcoin holdings in the future.”

Tesla isn’t in the bitcoin business, and neither are most companies. But hey, bitcoin can sit on balance sheets and act as a treasury asset for cash management if these companies so choose. Part of cash management means moving in and out of different assets as the needs of the business evolve.

Tesla, and other companies, will be back for more in due time.

Those off-base accounting rules governing digital assets

I promised to cover some off-base accounting rules, so I will because they’re somewhat important. It also aligns with my general view that “going public is dumb” and that “infinite growth is not only impossible, but bad.”

I’ll keep it brief.

Right now, bitcoin is treated as an indefinite-lived intangible asset. That means the companies that hold bitcoin on their balance sheets need to mark down its balance sheet value if bitcoin’s price decreases. This is sensible and gives an accurate representation of the financial reality that the asset it holds is now worth less.

Unfortunately, because bitcoin is treated as an indefinite-lived intangible asset, the company is not allowed to increase the value of the bitcoin to accurately represent the financial reality that the asset it holds is now worth more. Mark-to-market assets, in contrast, allow companies to adjust the value of an asset to reflect its value as determined by current market conditions. If bitcoin were allowed to be treated as a mark-to-market asset, companies could do this.

The rule that requires bitcoin to be treated as an indefinite-lived intangible asset is determined by the Financial Accounting Standards Board (FASB) in the U.S. And they should change the rule for two reasons.

First, it makes sense. Indefinite-lived intangible assets include things like goodwill, a made-up asset that allows acquiring companies to overpay for a target. Goodwill doesn’t trade on any sort of liquid market, but bitcoin does. Marking goodwill to market is basically impossible; marking bitcoin to market is easy.

And second, it would give a more accurate representation of companies’ financial positions. Public companies in the U.S. are already onerously tasked with providing quarterly financial reports to shareholders. If these companies hold bitcoin that is impaired one quarter and not allowed to be marked up the next, that will give an inaccurate representation of the company’s financial position without additional information from the company.

To that point, we should bring it back to Tesla. Remember it converted a majority of its bitcoin holdings for a gain offset by “impairment charges on the remainder of our holdings netting a $106 million cost to the [income statement].” So Tesla’s income statement doesn’t show the sale of bitcoin that made money (which is normal; it shows up on the cash flow statement), but it does show an income statement loss associated with bitcoin it didn’t sell. That makes no sense.

In the spirit of … ahem … making sense, perhaps we should start treating bitcoin like the mark-to-market asset it is.

You can get bonuses upto $100 FREE BONUS when you:

💰 Install these recommended apps:

💲 SocialGood - 100% Crypto Back on Everyday Shopping

💲 xPortal - The DeFi For The Next Billion

💲 CryptoTab Browser - Lightweight, fast, and ready to mine!

💰 Register on these recommended exchanges:

🟡 Binance🟡 Bitfinex🟡 Bitmart🟡 Bittrex🟡 Bitget

🟡 CoinEx🟡 Crypto.com🟡 Gate.io🟡 Huobi🟡 Kucoin.

Comments